Self-Employed vs Employee Status for Construction Workers: HMRC's Tests

- Atlas Tax

- Jul 7

- 13 min read

Self-Employed vs Employee Status for Construction Workers: HMRC's Tests in the UK

Whether a construction worker is genuinely self-employed or employed is determined by HMRC using the three-stage test from Ready Mixed Concrete (South East) Ltd v Minister of Pensions and National Insurance [1968]. The 2024 Supreme Court ruling in HMRC v PGMOL has updated how mutuality of obligation and control are assessed, and HMRC updated its Employment Status Manual in 2025 to reflect those changes. Getting the classification wrong can result in PAYE, employer NIC, and interest running back several years.

Why the Classification Matters So Much in Construction

A construction business regularly faces decisions about whether to engage workers as employees, under a labour-only subcontracting arrangement within CIS, or as genuinely self-employed individuals not within CIS at all. Each classification carries different tax and NIC consequences.

An employee: PAYE and employer NIC must be operated. Employer NIC in 2026/27 is 15% on earnings above the Secondary Threshold of £5,000 per year. The worker has statutory employment rights.

A self-employed worker under CIS: No PAYE obligation on the contractor for the worker's personal income tax, but CIS deductions of 20% (registered) or 30% (unregistered) must be applied to the labour element of payments. The subcontractor files a Self Assessment return and accounts for their own income tax and Class 4 NIC.

A genuinely self-employed worker outside CIS: No CIS obligation, no PAYE, no employer NIC. The worker is responsible entirely for their own taxes. This only applies where the work falls outside the scope of CIS altogether, which is a separate analysis.

HMRC's view is that where CIS applies, the registration and deduction requirements are mandatory regardless of whether the underlying relationship might also be challenged as employment. But a separate challenge can still be mounted claiming the individual was actually an employee, in which case the contractor faces both CIS liability and potential employment tax liability.

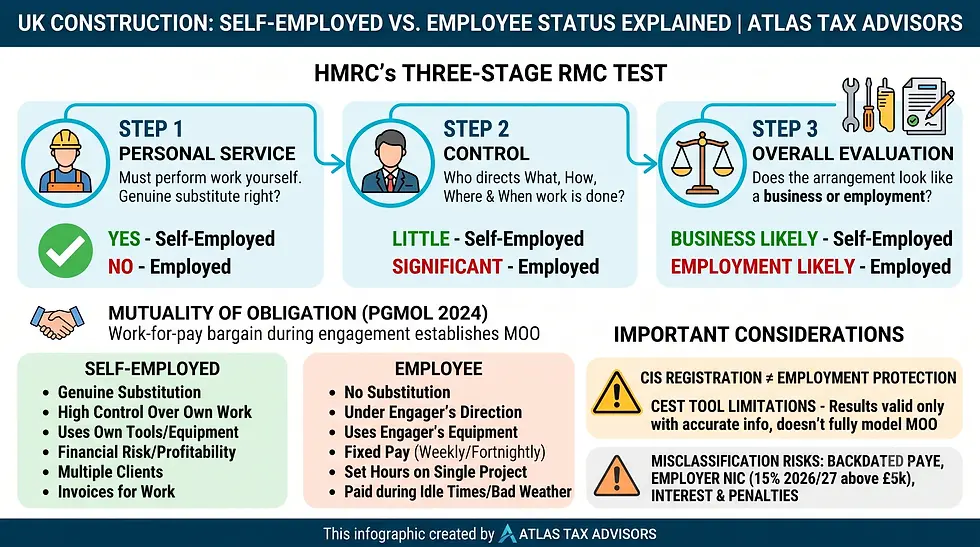

The Three-Stage Ready Mixed Concrete Test

The test is structured in three sequential stages, not as a list of factors to be weighed against each other. If a contract fails to satisfy any of the three conditions, it cannot be a contract of employment. The three conditions are:

First, the worker agrees, for remuneration, to provide their own work and skill in performance of the services. This is the personal service requirement.

Second, the worker is subject to a sufficient degree of control.

Third, other provisions of the contract are consistent with a contract of employment rather than a contract for services.

Only if the first two conditions are satisfied does the tribunal move to the third stage, which involves an overall evaluative exercise considering all the circumstances. The PGMOL Supreme Court ruling clarified both the first stage (mutuality of obligation) and the second stage (control).

HMRC updated its Employment Status Manual in 2025 to reflect these clarifications, adding a new section (ESM0560) on the evaluative exercise at the third stage.

Personal Service: Can the Worker Send a Substitute?

Where a worker has a genuine, unfettered right of substitution, meaning they can send someone else to do the work without needing the contractor's approval, there is no personal service obligation and the contract cannot be one of employment. In order to remove any requirement for personal service there should be a complete (or not unreasonably restricted) right to substitute personnel, or even to assign or subcontract the services to another party altogether.

For construction workers in practice, the substitution question is often the most practically decisive factor and the most commonly misunderstood one. A right of substitution must be genuine. A clause in a written agreement that says "the subcontractor may send a substitute" has limited value if in practice the worker has never exercised it, the contractor would not in reality accept a different individual, or the substitute would need to be someone from a small approved list.

HMRC is well aware of contractual substitution clauses inserted purely to create the appearance of self-employment. When investigating, HMRC looks at the actual working arrangements, not just what the contract says. A bricklayer in Milton Keynes working for the same main contractor for three years, arriving at the same site every day, using the site's equipment and following the site manager's instructions, will not be saved by a substitution clause if no substitute has ever been sent and the working practice looks nothing like genuine self-employment.

Where substitution rights are real and have been used, even occasionally, that is strong evidence of self-employment. The more restricted the substitution right (such as requiring the approval of the end client, or limiting substitution to only very specific circumstances), the weaker the indicator becomes.

Control: How Much Does the Contractor Direct the Work?

The second stage asks whether the engager exercises a sufficient degree of control over the work to be consistent with employment. This does not require control over every detail, but it does require a framework of control. The Supreme Court in PGMOL confirmed that what is required is "a right of control backed up with the possibility of imposing sanctions for poor performance," which is a broader concept than simply deciding exactly how each task is performed minute by minute.

In construction, control issues typically arise across three dimensions:

What work is done: where the contractor tells the worker which specific tasks to carry out each day, including assigning jobs within a project as needs arise, that points toward employment. A genuinely self-employed subcontractor more typically agrees a defined scope of work at the outset and delivers it without daily direction.

How and where: a worker told to use specific methods, attend a specific site at specified times, wear company branded clothing, and operate under the day-to-day oversight of the site manager is under a level of control consistent with employment. A subcontractor who owns their own tools and methods, decides their own working sequence, and is accountable only for the finished output is less controlled.

When: being required to work set hours on a schedule determined by the engager, rather than working to agreed milestones, points toward employment.

In practice, many construction working arrangements involve some control that looks like employment. A scaffolding subcontractor follows the project programme set by the main contractor. A groundworker operates under the supervision of the site manager for safety purposes. The question is whether the overall degree of control is consistent with employment, not whether any control exists at all.

Mutuality of Obligation: What PGMOL Changed

Mutuality of obligation (MOO) in its original formulation asks whether the engager is obliged to provide work and the worker is obliged to perform it. Where neither party has any obligation to the other between assignments, there is generally no continuing employment relationship.

The PGMOL Supreme Court ruling in 2024 clarified two things that had been contentious. First, it confirmed that MOO at the first stage of the Ready Mixed Concrete test is essentially the wage-work bargain: during any period when work is being done, the worker undertakes to work and the engager undertakes to pay. This is present in virtually any working arrangement. The absence of any obligation to offer or accept future work does not negate MOO during the period of actual work.

Second, the ruling confirmed that a right to withdraw from an engagement before it begins does not negate the MOO that exists once work has started.

HMRC had previously taken a simplified view that MOO is almost always present. The updated Employment Status Manual at ESM0543 now confirms the Supreme Court's position: the wage-work bargain during the engagement is sufficient for MOO to be established at stage one, without needing an overarching obligation to offer future work. This makes MOO harder to use as a standalone self-employment indicator in isolation, though the nature and extent of any obligations can still be considered in the evaluative exercise at stage three.

For construction workers, the practical implication is that arguing self-employment on MOO grounds alone, without also having strong evidence on substitution and control, is unlikely to succeed.

The Third Stage: The Overall Evaluative Exercise

Once personal service is established and a sufficient degree of control is found, the question becomes whether the totality of the arrangements is more consistent with employment or self-employment. This is not a mechanical checklist but an evaluative exercise looking at all the circumstances.

Factors that point toward self-employment in a construction context include: ownership of and investment in significant tools, plant or equipment; financial risk if the work is completed poorly or late; multiple engagements with different contractors in the same period; registration as self-employed with HMRC; provision of one's own insurance; invoicing for specific work rather than receiving a weekly wage; and a genuine ability to profit from efficiency in completing the work.

Factors pointing toward employment include: working for one engager over an extended period at a fixed rate; being directed by the engager's own employees; using equipment and materials supplied by the engager; being paid weekly or fortnightly as a regular wage; working regular hours set by the engager; and receiving pay even during idle periods or inclement weather.

Where the overall picture is mixed, as it often is in construction, no single factor is determinative. The tribunal conducts an overall assessment rather than counting indicators on each side.

HMRC's CEST Tool and Its Limitations

HMRC's Check Employment Status for Tax (CEST) tool is the official online route for assessing status. HMRC's position is that it will stand by CEST results provided the information entered accurately reflects the actual working arrangements.

However, CEST has been criticised for not properly reflecting the full range of case law nuances, including mutuality of obligation. A small MOO gateway question was inserted in May 2025, but the tool still does not model MOO as comprehensively as case law requires. This means CEST results can sometimes point toward self-employment even where a tribunal would reach a different conclusion on a full assessment of the facts.

Using CEST to confirm self-employment status provides some protection only where the information entered is accurate. Where the actual working practices diverge from what was entered into the tool, the result is worthless as a defence.

CIS, Employment Status, and the Overlap

An important practical point is that CIS compliance and employment status are separate questions. A worker can be a registered CIS subcontractor and still be reclassified as an employee by HMRC if the actual working arrangements are sufficiently employment-like.

CIS registration does not protect the contractor from an employment status challenge. Where HMRC reclassifies a CIS worker as an employee, the contractor faces PAYE and employer NIC liability on the payments made, less any credit for CIS deductions already remitted. If reasonable care has not been exercised, HMRC is able to recover tax from six years earlier, together with interest and potential penalties.

The risk is highest where a construction business has workers who have been on site for extended periods, work exclusively for that one business, and whose working arrangements look substantially like those of employed site workers. These arrangements are exactly the profile HMRC's Construction Industry Compliance team focuses on.

Key Takeaways

HMRC applies the three-stage Ready Mixed Concrete test: personal service (including substitution), control, and whether other provisions are consistent with employment. If any of the first two stages fails, there cannot be employment, regardless of other factors.

The PGMOL Supreme Court ruling in 2024 confirmed that mutuality of obligation is present whenever work is done for payment, and that the right to withdraw before starting does not negate it. HMRC updated its Employment Status Manual in 2025 to reflect this.

In construction, the most practically decisive factors are usually the right of substitution and the degree of control. A genuine, exercised right to send a substitute provides strong evidence of self-employment. Workers who follow daily site instructions, use the contractor's equipment, and work set hours are demonstrating significant control consistent with employment.

CIS registration does not protect a contractor from an employment status reclassification. Both CIS obligations and employment tax obligations can apply simultaneously.

CEST can be used to assess status, but HMRC only stands behind the result where the information entered accurately reflects the actual working relationship.

Where the facts suggest misclassification, voluntary disclosure and a careful review of current arrangements is preferable to waiting for HMRC to open a formal compliance check.

FAQs

Q1: How does working for multiple contractors in the construction industry affect your employment status under HMRC rules?

In my experience advising construction clients across the UK, this is one of the most common grey areas. If you're genuinely able to turn down work from one contractor and take jobs from others without repercussions, provide your own tools, and quote a price for the full job rather than an hourly rate, it strongly supports self-employed status. Consider a bricklayer in Manchester who juggles three different firms in a month, invoices each separately, and absorbs the cost if materials run over, that level of financial risk and freedom usually points away from employee status. However, if one main contractor dictates your schedule and methods even while you pick up occasional side work, HMRC might view the dominant relationship as employment. Always document your different engagements clearly for your records.

Q2: What happens if a construction worker is misclassified as self-employed when they should be on PAYE,and who bears the cost?

This is a classic pitfall I've seen trip up many building firms and their subcontractors. If HMRC determines "false self-employment," the contractor (the engager) typically becomes liable for the unpaid employer's National Insurance, plus interest and penalties, while the worker might face adjustments to their tax position. For instance, I've had a client in Birmingham whose scaffolder was treated as CIS-registered for two years; when reviewed, the working practices showed too much control by the firm, leading to a substantial back-payment bill for the contractor. The key takeaway? Don't rely solely on CIS registration, review the actual day-to-day reality using HMRC's factors like control and substitution.

Q3: Can someone in construction switch from employee to self-employed status mid-project, and what precautions should they take?

Switching is possible but requires careful handling to avoid challenges. In practice, I've guided clients through this by ensuring a clear break in the relationship, new contract terms, different payment structures, and genuine changes in how the work is performed. A plasterer I advised in Glasgow finished an employed phase on one site and then tendered for the next phase as a subcontractor with his own insurance and the ability to send a mate in his place. Document everything in writing and consider running it through HMRC's CEST tool for reassurance. Remember, HMRC looks at the substance over any labels you apply.

Q4: How do Scottish income tax rates interact with self-employed status for construction workers compared to the rest of the UK?

Scottish residents pay different income tax bands, which can make a noticeable difference for higher-earning self-employed tradespeople. While National Insurance remains the same UK-wide, the starter rate and additional bands in Scotland might mean slightly lower or higher effective tax depending on your profit level. I've seen electricians in Edinburgh benefit in lower bands but feel the pinch higher up compared to colleagues down south. As a self-employed person, you'll handle this via Self Assessment, so good record-keeping of expenses is even more vital to manage cash flow across the year.

Q5: What role does the ability to provide a substitute play in determining self-employed status for a construction subcontractor?

This is a powerful indicator in HMRC's eyes. If you can send a qualified replacement to complete the job without the contractor's approval being needed for the person (as long as the work meets standards), it leans heavily towards self-employment. In one case with a roofing client in Leeds, the ability to sub out work during busy periods or illness helped solidify his status during a review. Without that right in practice, even if mentioned in a contract, it weakens your position. Make sure your agreements reflect real flexibility here.

Q6: Does operating through a limited company automatically protect construction workers from employment status disputes under IR35?

Not at all, this is a common misconception. For off-payroll working rules (IR35), the engager often determines status, especially in larger contracts. If the working practices resemble employment, you'll be taxed similarly to an employee anyway, with deductions at source. I've advised many specialist tradespeople who assumed their LTD setup offered full protection, only to face reclassification risks. Use the CEST tool tailored to your specific engagement and maintain proper corporate governance to strengthen your case for being outside IR35.

Q7: How should construction business owners handle employment status when hiring agency workers or those with heavy plant equipment?

Agency workers often default to different rules, but for those supplying their own expensive equipment, it can support self-employed arguments due to financial investment and risk. However, if the agency or main contractor still exercises significant control over methods and hours, status can shift. A groundwork contractor I worked with in the South West hired operators with their own machinery; clear contracts emphasising the hirer's autonomy helped, but we still reviewed each arrangement. Always verify with proper due diligence rather than assuming equipment ownership alone decides it.

Q8: What are the implications for pensions and benefits when a construction worker is self-employed versus employed?

Self-employed individuals have more flexibility but also more responsibility. You won't get automatic employer pension contributions, so planning your own SIPP or personal pension is crucial, especially with variable income common in trades. On the flip side, employed status brings Statutory Sick Pay and holiday entitlements that self-employed miss out on. I've seen brickies regret not setting aside for pensions early; a simple monthly contribution habit can make a huge difference come retirement. Check your National Insurance record too, as gaps can affect state pension forecasts.

Q9: If a construction subcontractor has both PAYE income from one job and CIS payments from others, how does this affect their overall tax position?

This hybrid situation is increasingly common and requires careful Self Assessment reporting. The PAYE income is taxed at source, but CIS deductions are treated as payments on account against your self-employed profits. Over-deduction via CIS can lead to refunds, but under-declaration risks penalties. One client, a joiner splitting time between a large firm (PAYE) and private jobs (CIS), nearly missed claiming allowable expenses on the self-employed side, which would have cost him dearly. Track everything separately and consider quarterly planning to avoid nasty surprises.

Q10: What practical steps can high-earning self-employed construction workers take to future-proof against HMRC status reviews?

For those earning well, the stakes are higher, so proactive habits pay off. Maintain detailed contracts for every job highlighting self-employed features (fixed price, substitution rights, own equipment), keep impeccable records of expenses and multiple clients, and periodically run the CEST tool. In my practice, clients who treat their trade like a proper business, with separate bank accounts, insurance, and marketing,fare much better in any scrutiny. It's not about ticking boxes but genuinely running things that way. If in doubt, seek tailored advice for your specific setup, as every situation has unique nuances.

Disclaimer

The information published on the above article is provided for general informational and educational purposes only. Although reasonable care is taken to ensure that the content is accurate, current and based on reliable sources at the time of publication, UK tax law, HMRC guidance, rates, thresholds and compliance requirements may change, and their application can vary depending on individual or business circumstances. Nothing on this blog constitutes personalised tax, accounting, financial, legal, immigration, investment or professional advice, and it should not be relied upon as a substitute for advice from a qualified professional adviser. Readers should seek tailored advice before making decisions, submitting returns, claiming reliefs, entering transactions, or taking or refraining from any action based on blog content.

Atlas Tax Advisors, its directors, CEO, employees, consultants, contributors, authors, editors and content creators accept no liability for any loss, penalty, interest, damage, claim, cost or consequence arising directly or indirectly from reliance on, interpretation of, or use of any information contained in these blog posts, to the fullest extent permitted by UK law. External references, examples and scenarios are illustrative only and do not create a client relationship. A professional relationship with Atlas Tax Advisors is formed only through formal engagement and agreed terms of service.

Comments